How To Use Your Texas Home Equity to Avoid Foreclosure

Home foreclosure can happen to the best of us, even here in Texas. Unexpected job and financial circumstances can put us in a tough place, and it might seem like going into foreclosure is your only option when you can't pay your mortgage... but it's not!

Home foreclosure can happen to the best of us, even here in Texas. Unexpected job and financial circumstances can put us in a tough place, and it might seem like going into foreclosure is your only option when you can't pay your mortgage... but it's not!

You have other options that will help you avoid foreclosure in Texas. First, we'll share what we feel is the best route to take: Selling your Texas home. Especially while we are still in a Seller's Market.

Molly Boesel, Principal and Economist from CoreLogic puts it plainly:

In contrast to the financial crisis, when roughly 25% of borrowers were underwater, most borrowers today who are behind on mortgage payments can tap into their equity and sell their home rather than lose it through foreclosure. (emphasis added)

Let's take a look at what this means and how it works.

How To Use Your Texas Home Equity to Avoid Foreclosure

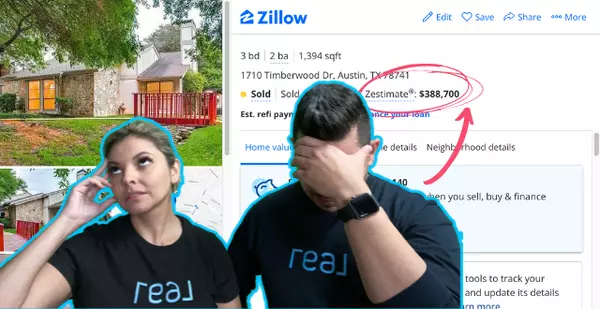

Before you pursue any complicated methods for avoiding foreclosure in Texas, it’s worth seeing if you have enough equity in your home to sell it and protect your investment. A quick home value report will give you a general idea of how much equity you might have.

Put simply, equity is the difference between what you owe on your home and its current market value.

In today’s Texas real estate market, many homeowners have way more equity in their homes than they think. Over the last year, buyer demand has been high, but housing supply has been low. That’s led to a BIG increase in home values.

Because when prices rise, so does the amount of equity you have in your house.

On average, homeowners gained $33,400 in equity over the last 12 months (source: CoreLogic). See the map below:

Keep in mind, if you live in the Austin area or near one of the major metro areas in Texas, your home equity may be much higher than the map shows.

So, what does that mean for you?

Over the past year, chances are your home’s value (and therefore your equity) has risen dramatically. If you’ve been in your home for a while, the mortgage payments you’ve made over time chipped away at the balance of your loan.

If your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage.

To find out what your house is worth in today’s market, it's as easy as filling out a free Home Value Report (takes about 2 minutes). Once submitted, we'll reach out to give you a more customized valuation and help with next steps.

If you are thinking of selling your home or would like to chat about your options, contact us here, and be sure to check out our video where we go into detail about all of your options to avoid foreclosure:

Other Options to Avoid Foreclosure in Texas

If you find out that you have to pursue other options, we can help with that too. We're happy to connect you with other professionals in the industry, who can look into your unique situation and offer advice on next steps if selling isn’t the best alternative.

1) Loan Reinstatement

Federal law requires that lenders wait 120 days before starting the foreclosure process. If you are able to pay the total amount past due from your missed payments BEFORE this time period ends, you can avoid foreclosure.

The loan reinstatement (also called the mortgage reinstatement) process provides an option to avoid foreclosure by allowing you to catch up on your payments and cover any late fees to restore the mortgage.

Once you are caught up, the defaulted mortgage will receive a clean slate, and you will continue to make regular monthly mortgage payments.

2) Loan Modification

Investopedia describes loan modification this way:

Loan modification is a change made to the terms of an existing loan by a lender. It may involve a reduction in the interest rate, an extension of the length of time for repayment, a different type of loan, or any combination of the three.

Most experts recommend that you reach out to an attorney or a settlement company to assist with your loan modification negotiations.

3) Opt for a Short Sale

In a short sale, you sell your home for less than the balance remaining on your mortgage.

You should call your mortgage servicer to explain your situation and ask if this is an option. If they agree to a short sale, you can sell your home and pay off the necessary amount with the profit from the sale.

Once the short sale is complete you’ll be relieved of your responsibility to pay any remaining balance—called a “deficiency waiver.”

Next Step

If you are facing hardships, live in the Texas, we can help. Reach out anytime.

Categories

Recent Posts

GET MORE INFORMATION

Victor A Aguilar

Agent/Team Lead | License ID: 0653089

Agent/Team Lead License ID: 0653089